It's Presidential election season time and, once again, as has been the case for nearly 30 years, it's the time when sophisticated, discerning undecided voters pose the tough questions to the Presidential candidates and the rest of us get to decide who knows less --- the undecideds or the candidates. Probably the top question posed during election season that shouldn't be involves how each candidate envisions "doing something" about the price of gas.

It really helps to look at some graphs before explaining how naive the question really is.

Worldwide oil production from 1980-2012:

http://www.indexmundi.com/energy.aspx?product=oil&graph=production

Worldwide oil consumption from 1980-2012:

http://www.indexmundi.com/energy.aspx

North American oil consumption from 1980-2012:

http://www.indexmundi.com/energy.aspx?region=na&product=oil&graph=consumption

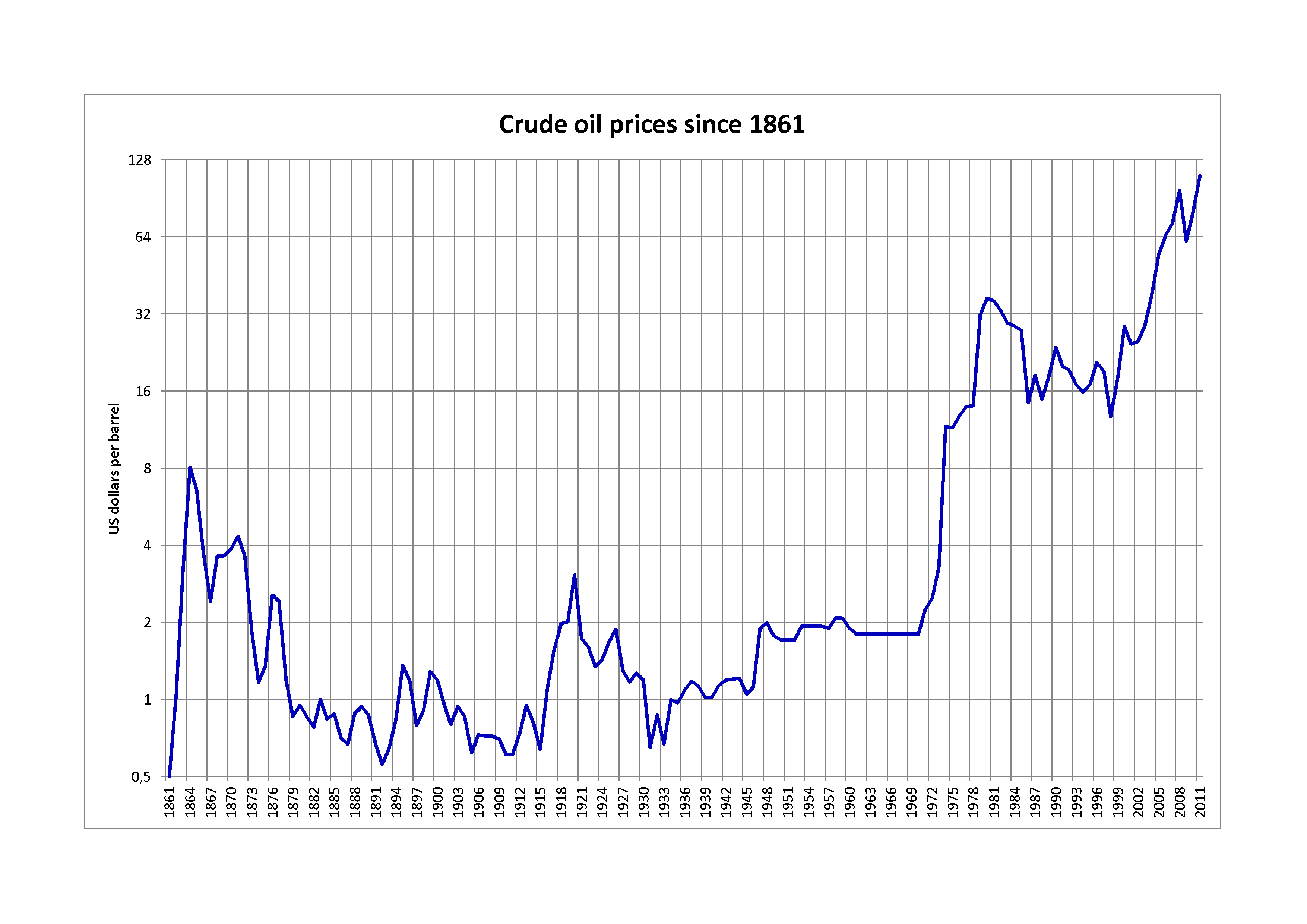

Oil prices from 1861 to 2012:

http://upload.wikimedia.org/wikipedia/commons/8/82/Crude_oil_prices_since_1861_%28log%29.png

These graphs suggest the following critical conclusions:

* oil demand worldwide grew from 59.9 million barrels/day in 1980 to

86.9 million barrels/day in 2010 in pretty much a straight line -- about

45 percent growth over 30 years

* oil demand in North America has grown since 1980 but only by 25% from 1980

to the peak in 2005

* oil demand in North America has actually dropped since 2007, partly because

of the recession but also due to improved efficiency

* worldwide production has kept up with demand outside of coordinated

embargoes

* oil prices have jumped ALL OVER from roughly $24/barrel in 1980

to over $100/barrel with eight different spikes or drops of 50%

or more since 1980

Suppose you are a free market purist and believe prices are a reflection of supply and demand. If North American demand has only grown about 25 percent over 30 years and has actually dropped a bit for the last five, why would oil prices have gone up over 400 percent over the same period? If both supply and demand have been inching upward steadily over the entire period, what could possibly produce eight different spikes or drops in price of over 50 percent over that period?

The answer boils down to three factors:

1) America isn't the only one buying oil every day on the open market

2) Most oil contracts are denominated in US dollars, given the US dollar's

role as the world's reserve currency

3) Oil has become yet another vehicle of speculators trying to score

big profits from volatile prices

Since the early 1990s, the exponential growth of the Chinese economy has contributed most of the growth in worldwide demand for oil. When another player shows up wanting to buy nearly as much oil as the current players on the market, any slack in the market that would otherwise keep prices down during slight dips in demand never occurs, keeping upward pressure on prices.

The US dollar's status as the world's reserve currency also tends to exaggerate rather than smooth the effective price of oil. The US dollar itself is a commodity because many international contracts are denominated in dollars, especially oil contracts. That means two non-American countries wanting to buy oil must typically first buy US dollars with their local currency, then use the US dollars to buy the oil they need. That means foreign buyers of oil wind up speculating to some degree in TWO commodities and get exposed to two risks -- fluctuations in exchange rates into the dollar which can swing widely due to financial concerns within the US or abroad and fluctuations in the oil markets, which then get priced in fluctuating US dollars.

During a period when demand for oil seems relatively predictable and new production techniques seem to be keeping up with demand, what else could cause oil prices to fluctuate so wildly? Simply put, after investors chased bubbles in technology stocks in the late 1990s to a crash, then chased real estate assets in the 2000s until the crash in 2007, oil became the next haven of speculators and hedge funds trying to make up profits lost in other sectors. The US was at war in the mid-east, the economies of several large countries were nearing complete economic collapse so the possibility of a supply interruption seemed to make sense to many, helping to rationalize a spike up in prices. However, this took place at the time the larger worldwide economy was collapsing, something that itself would have normally dropped oil prices. Eventually, reality kicked in, triggered a panic, and dropped oil prices FAR below long term price points associated with a worldwide economy not contracting at 2-5 percent annually.

Stated more simply, if supply and demand were the primary drivers of oil price fluctuations, consistent upward growth in worldwide demand with matching upward growth in supply would never produce 50 percent DROPS in price. Those types of fluctuations can only be produced by other factors, none of which have anything to energy regulation or marginal tax rates and special credits for producers. Since oil itself is a fungible worldwide commodity, there's nothing any American President

-- of either party -- can do or needs to do to alter regulations or tax policies to affect prices. As long as the portion of the world wanting to enjoy the hydro-carbon fueled good life as much as America does continues growing, America will have little control over oil prices. The only way to lessen the headaches from the up-and-down rollercoaster of oil prices is to get off the ride ASAP and adopt other energy sources more under our control and less subject to manipulation and speculation.

{kind=link}